Audit Procedures: Definition, Methods, & Types

This guide will discuss: what are audit procedures, its methods, and types. Additionally, discover which of the following audit procedures is the most reliable source of audit evidence.

This guide will discuss: what are audit procedures, its methods, and types. Additionally, discover which of the following audit procedures is the most reliable source of audit evidence.

Published 28 Apr 2026

Article by

6 min read

Audit procedures are the techniques, processes, and methods that auditors use to obtain reliable audit evidence, which enables them to gain a sound judgment about an organization’s financial status. Audit procedures are conducted to help determine whether or not a company’s financial statement is credible and factual. The regular implementation of these procedures helps establish a business’s financial reputation and strengthen its trustworthiness in the eyes of its customers, the market, and potential investors.

There is no definitive structure when it comes to auditing; its whole process would depend on the auditor, the company to be audited, and the purpose of the audit. Learn more about the two main methods of audit procedures below:

Substantive methods are audit processes that provide actual physical evidence including paper trails such as financial statements, books of accounts, or transaction records. This also includes other important documents such as registry for land or deed/agreement for the building rent. Essentially, substantive methods include any tangible proof that not only provides a conclusive understanding of the circumstances, but also has a high level of accuracy.

While the substantive method uses apparent proofs as an audit basis, analytical methods take this a step further. Analytical methods pair financial data with non-financial data and determine the correlation between them. Comparison of previous trends vs current trends, as well as evaluation of the difference between the client’s record and the substantive evidence, are also considered analytical methods.

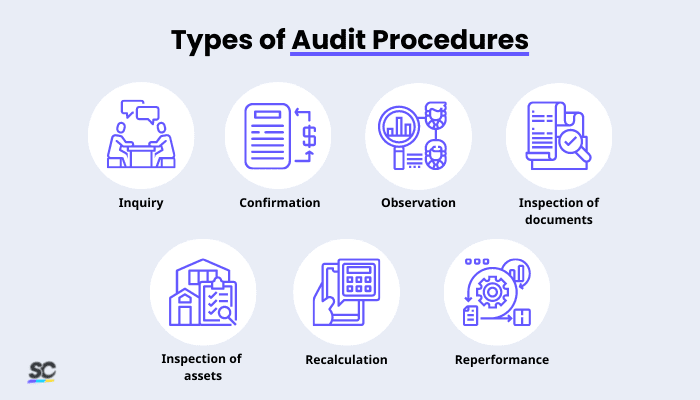

During the planning phase of an audit for a company, it is a requirement to perform a risk assessment to understand the environment of the organization, as well as to recognize its weaknesses and to identify the best set of audit procedures to use. Audit procedures include inquiry, confirmation, observation, inspection, recalculation, and reperformance. Know more about each of them:

One of the simplest types of audit procedures is inquiry. This procedure involves auditors collecting verbal evidence through formal or informal inquiry from the people in the organization. Although relevant, this type of evidence isn’t strong enough to stand alone and would need other supporting documents or proofs to be considered valid.

Similar to inquiry, confirmation also asks for explanations regarding the transactions of an organization. The main difference, however, is that auditors would validate them through direct communication with a third party or other external sources that an organization has relationships with. Examples of these third parties are banks, suppliers, or customers.

With this type of audit process, auditors usually try to confirm that existing business procedures or measures are being implemented by the organization. This type of procedure gives auditors an idea on how internal processes work, and if they can affect the operations of the organization as a whole.

Inspection of documents is the process of gathering and examining transactions through recorded information. This can be performed using two ways—vouching and tracing.

Vouching is where auditors manually check the details of supporting documents to verify the transaction records. Meanwhile, tracing is the process of validating transactions by tracking their connections to the source document.

Inspection of tangible assets is the procedure where auditors physically examine the company’s assets including properties such as land, building, vehicles, equipment, or inventory. This process doesn’t only confirm the existence of the asset, but also helps in determining whether it suffered defects or impairment, which affect its value.

Auditors can make a list of all the fixed assets of a company or use this asset register checklist for the inspection.

Build from scratch or choose from our collection of free, ready-to-download, and customizable templates.

This audit process is fairly straightforward. In recalculation, auditors recompute the transactions themselves and compare them to the initial financial statement or calculation of the company. Auditors can then identify if they are balanced, or further investigate if there are any differences or discrepancies found.

Reperformance is simply just auditors independently repeating the audit procedures or internal controls the company has also performed. Audit evidence obtained using this procedure is considered more reliable than evidence indirectly gathered, because it’s a first-hand experience and direct form of evaluation.

Auditors can always perform their audits using multiple procedures. For example, aside from just checking supporting documents, they can also inspect physical assets or ask other related third parties for confirmation of existing transactions. By performing various audit procedures, auditors can strengthen the credibility of the audit result and reduce the chance of miscalculations and discrepancies.

Although the above-mentioned procedures all have their own benefits, which of them are considered to be the most reliable?

According to this article from Chron, physical inspection, confirmation from a third party, and inspection of records and documents are considered three of the most reliable audit procedures. Aside from them offering highly accurate information, they are also backed by audit evidence that is easy to double-check and validate.

These audit procedures also enable auditors to independently examine on their own and not just rely on the information that a company has given. This helps ensure that audit results are unbiased and as accurate as possible.

Regardless of which audit procedures and auditing tools are chosen, it is essential to encourage organizational collaboration and teamwork. It is important that everyone in an organization is aware of how it works from the top down. With mobile learning management systems or LMS like SafetyCulture (formerly iAuditor)’s Training, you can create, test, and deliver deploy mobile courses to guarantee to ensure that your teams are in the loop and comply with your standards in process improvement.

Continuous improvement fails when people miss real work. Bridge the gap today with a digital tool that helps teams act on what truly matters.

SafetyCulture is a digital auditing platform that both businesses and auditors can use in performing several auditing procedures. Aside from risk assessments, you can also utilize SafetyCulture to inspect your physical assets using this asset register checklist, or download and use other relevant templates from the Public Library. Streamline your auditing process with SafetyCulture and do the following:

Create and customize your own checklists or templates to use in the audit process.

Monitor and track your auditing process with the analytics dashboard.

Train employees on proper auditing procedures.

Manage assets as they are used for a more effective auditing process.

Attach photo evidence to your asset inspection for high-level visibility.

Document asset impairment by reporting them as issues.

Generate inspection reports automatically and share them with all involved people via email, PDF, or web link.