Understanding Internal Control Frameworks: The Cornerstone of Risk Management

Learn everything about internal control frameworks: benefits, key components, and best practices to strengthen your organization’s governance and risk management.

Learn everything about internal control frameworks: benefits, key components, and best practices to strengthen your organization’s governance and risk management.

Published 28 Apr 2026

Article by

5 min read

An internal control framework is a structured system of policies, procedures, and practices that ensure the organization’s operations are effective, aligned with its objectives, and compliant with regulations and industry standards. There are several established frameworks to choose from, depending on organizational needs. Each aims to minimize risks, maintain accountability, and foster stakeholder confidence.

Checks and balances, one of the most rudimentary of internal controls, have been implemented for centuries to prevent fraud and theft in trade and treasury systems. The need for stricter controls was emphasized in the 21st century due to the growing complexities in business systems and controversial financial reporting scandals. Here are its specific benefits:

Enhanced risk management – Fraudulent activities, irregularities, and other risks are immediately identified, allowing relevant personnel to execute the planned corrective or preventive action.

Improved operational efficiency – With a clear and well-defined roadmap, companies can delegate roles and responsibilities appropriately, optimize processes, and improve overall productivity.

Increased cost savings – Aside from reducing waste by streamlining workflows, organizations won’t have to use up resources on errors, inefficiencies, fraud, and their subsequent legal challenges.

Higher levels of accountability and transparency – Ethical practices based on internal control frameworks help companies meet industry-specific regulatory requirements. It also builds stakeholder trust—vital for business sustainability.

Ensured business continuity – Continuously monitoring internal controls prepares organizations to handle disruptions and unforeseen challenges. High levels of adaptability drive resilience in the face of constantly emerging risks.

Centralize policies and procedures to maintain consistency, reduce compliance risks, and ensure governance strategies align with organizational goals.

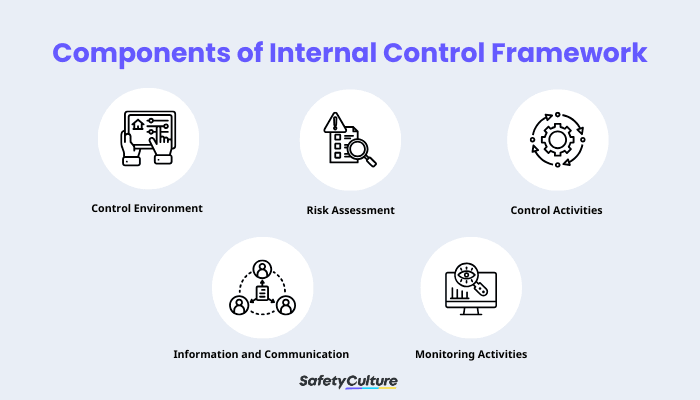

The success of an internal control framework lies in five interconnected components. These must function cohesively and be considered when integrating a specific framework into the system. These are the components of internal control framework:

Components of Internal Control Framework

As the foundation setter, the control environment establishes the organizational culture, values, and ethical standards. When designing the framework, the senior management should set clear objectives to promote a culture of accountability and responsibility across all organizational levels. For this component, apply these best practices:

Gain leadership buy-in, particularly for support on allocating resources and setting standards.

Review the organizational structure to assign specific roles and responsibilities.

Develop training programs to improve employee competency and encourage autonomy and ownership of their work.

One of the most invaluable elements of internal controls, carefully assessing risks enables department heads to proactively address the vulnerabilities and emerging threats before they cause more turmoil in the organization. Here are some of the most common threats:

Operational risks – process errors, system failures, lack of training

Financial risks – credit defaults, cash flow dry-up, foreign exchange fluctuations

Human resources risks – employee turnover, misconduct

Economic risks – recession, inflation

Competitive risks – new entrants, changing customer demands

Regulatory risks – changing laws, new compliance requirements

Environmental risks – natural disasters, climate change, pollution

Implementing a risk-based approach helps assess the likelihood, impact, and severity. It’s beneficial for organizations that may not have a lot of resources to shell out.

Build from scratch or choose from our collection of free, ready-to-download, and customizable templates.

Policies, procedures, and mechanisms address and mitigate the risks identified. To design effective controls, take note of the following best practices:

Tailor the controls, implementing a mix of preventive and detective controls.

Segregate duties, separating authorization, execution, recording, custody, and reconciliation functions to minimize errors and the possibility of fraud.

Integrate software solutions to automate routine tasks and improve efficiency.

Timely and accurately disseminating relevant information ensures everyone understands their role in maintaining internal controls and adhering to policies. Consider the following practices to maintain transparency:

Open channels for communication across departments, preventing silos that result in duplicated efforts or loss of productivity.

Make policies and procedures accessible to everyone involved.

Include external stakeholders in the process, including third-party auditors and government regulators.

Ongoing assessments and evaluations ensure internal controls remain effective over time, can adapt to changing circumstances, and address any emerging risks. Often disregarded for lack of resources, constant monitoring is one of the most vital internal control framework components because it addresses the following challenges:

Inefficiencies in business processes that require adjustments

Fraud, errors, and irregularities

Possible mistrust from stakeholders, particularly after failing controls

Organizations across industries should implement three categories of internal controls to ensure extensive risk protection and mitigation. Here are the different kinds and corresponding examples to consider for a structured internal control framework:

Proactive measures establish barriers or safeguards to minimize the risk of undesirable events, such as errors and fraud. Some common frameworks under this category include the following:

The COSO (Committee of Sponsoring Organizations of the Treadway Commission) framework emphasizes the need for risk assessment and control activities.

ISO 31000 established by the International Organization for Standardization (ISO) focuses on a proactive approach to risk management. This can be a launching point for more targeted risk management frameworks.

This type of control identifies and alerts organizations about errors or irregularities after they have occurred. Here are some examples:

The NIST (National Institute of Standards and Technology) cybersecurity framework monitors and detects critical components of cybersecurity.

The COBIT (Control Objectives for Information Technologies) provides guidelines for managing IT governance to detect issues within IT processes.

These come into play after issues have been identified, rectifying deficiencies and preventing future occurrences of similar problems.

ITIL (Information Technology Infrastructure Library) offers a set of practices to efficiently resolve incidents based on detected issues.

Lean Six Sigma is a process improvement framework that identifies defects and implements corrective actions.

Unlock hidden efficiency

Middle managers lose over 5 hours each week on low-value tasks—time that could be spent driving meaningful progress. Learn why they hold the key to operational success.

SafetyCulture is a mobile-first operations platform adopted across industries, such as manufacturing, mining, construction, retail, and hospitality. It’s designed to equip leaders and working teams with the knowledge and tools to do their best work—to the safest and highest standard.

Streamline and standardize workflows to improve efficiency and productivity in assessing risks, identifying vulnerabilities, and implementing appropriate controls. Increase inter-team collaboration, removing silos that may result in errors, fraud, and non-compliance. Enable monitoring to facilitate continuous improvements across departments through a unified platform.

✓ Save time and reduce costs ✓ Stay on top of risks and incidents ✓ Boost productivity and efficiency ✓ Enhance communication and collaboration ✓ Discover improvement opportunities ✓ Make data-driven business decisions