What Is a SOX Compliance Audit?

A SOX compliance audit is a formal evaluation of a public company's internal controls over financial reporting (ICFR) against the requirements of the Sarbanes-Oxley Act. It verifies that controls are properly designed, operating effectively, and supported by sufficient evidence to satisfy both management's own assessment and independent external auditor attestation.

Who Must Comply — and How Often

SOX applies to all US-listed public companies, foreign private issuers with securities registered on US exchanges, and certain third-party financial service providers to those entities. Private companies preparing for an IPO typically begin building SOX-compliant control environments 12–18 months before listing.

The fiscal year-end reporting timeline drives the annual SOX compliance audit cycle. Most organizations operate on a continuous compliance calendar: scoping and walkthroughs early in the year, control testing through mid-year, interim-to-year-end roll-forward updates, and management assessment and external auditor attestation in the final quarter.

SOX 302 vs. SOX 404: Key Differences

These are the two sections that define the bulk of audit work:

| Section 302 | Section 404 |

What it requires | CEO and CFO personal certification that financial statements are accurate and that disclosure controls and procedures are effective | Management's annual assessment of ICFR effectiveness, plus independent auditor attestation (for accelerated filers) |

Scope | Disclosure controls and procedures broadly | Internal controls specifically over financial reporting |

Evidence required | Signed certifications filed with each 10-K and 10-Q | Documented control design, operating effectiveness testing, deficiency evaluation, and management report |

External auditor role | Auditor reviews but does not separately attest | Auditor independently tests and issues opinion on ICFR effectiveness (PCAOB AS 2201) |

Frequency | Each annual and quarterly filing | Annual |

Scoping Your SOX Audit

Scoping determines which entities, processes, accounts, and controls fall within the audit boundary. Over-scoping wastes resources; under-scoping creates compliance risk. The SEC recommends a top-down, risk-based approach (TDRA) for scoping decisions.

Materiality and Qualitative Risk Factors

Quantitative materiality is typically calculated as a percentage of pre-tax income, total assets, or revenue — commonly 5% of pre-tax income for planning materiality. Significant accounts and disclosures are those with a reasonable possibility of containing a misstatement that exceeds this threshold.

Qualitative factors can bring accounts or processes into scope regardless of dollar size, including: susceptibility to fraud, recent changes to the process or system, complexity of the accounting treatment, and management judgment involved.

Identifying Key Controls

Not every control in a scoped process is a "key control" for SOX purposes. A key control is one that, if it failed, would allow a material misstatement to go undetected or uncorrected. The documentation should explicitly state why each control is designated as key versus non-key, and what assertion(s) it addresses (completeness, accuracy, existence, valuation, presentation and disclosure).

Entity-level controls (ELCs) — including tone at the top, governance structures, risk assessment processes, and monitoring activities — should be evaluated first, as effective ELCs may allow for a reduction in the scope or precision of process-level testing.

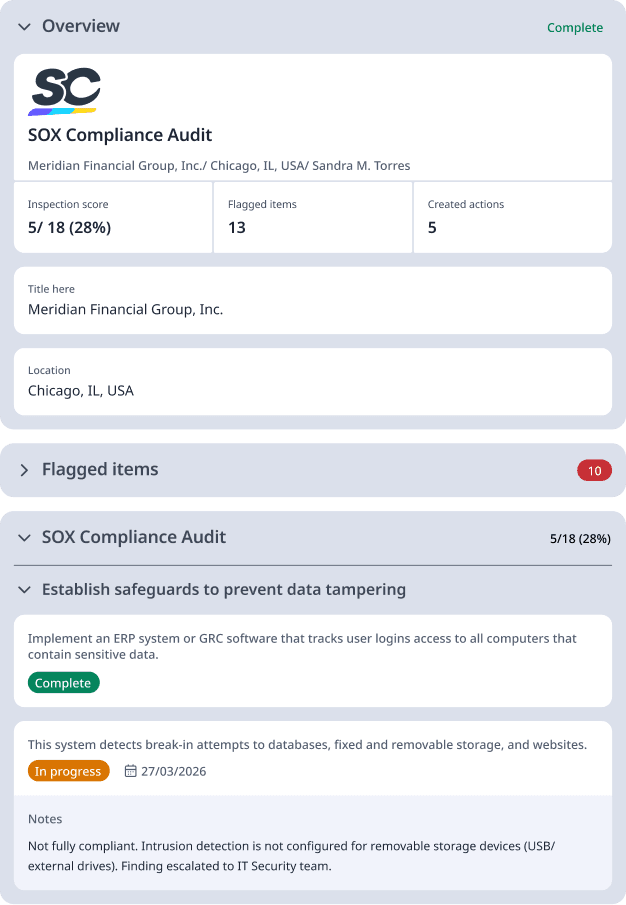

What to Include in a SOX Compliance Audit Checklist

A SOX (Sarbanes-Oxley Act) compliance audit ensures that public companies maintain accurate financial reporting and robust internal controls. The checklist below covers the key areas auditors and compliance teams must evaluate to meet SOX requirements.

Entity-Level Controls — Assess the overall control environment, including management's tone at the top, code of conduct policies, whistleblower programs, and the board/audit committee's oversight responsibilities.

Risk Assessment Process — Document how management identifies, analyzes, and responds to financial reporting risks, including fraud risks and changes in business operations that could affect internal controls.

Financial Close & Reporting Process — Review the end-to-end financial close process, including journal entry controls, account reconciliations, and the accuracy of financial statements and disclosures.

Access Controls & IT General Controls (ITGCs) — Evaluate user access management, segregation of duties, privileged access, password policies, and controls over key financial systems (ERP, databases, etc.).

Change Management Controls — Verify that changes to IT systems, applications, and infrastructure follow a formal approval, testing, and documentation process to prevent unauthorized modifications.

Segregation of Duties (SoD) — Confirm that no single individual has end-to-end control over a critical financial process (e.g., the same person cannot both initiate and approve a payment).

Revenue Recognition Controls — Examine controls around how revenue is recorded, ensuring compliance with applicable accounting standards (ASC 606) and that cutoff procedures are properly applied.

Accounts Payable & Procurement Controls — Review purchase order workflows, invoice approval processes, vendor management, and three-way matching to prevent unauthorized payments.

Payroll Controls — Assess controls over payroll processing, including authorization of new hires/terminations, timesheet approvals, and segregation between payroll setup and disbursement.

Financial Reporting & Disclosure Controls — Confirm that management review controls (MRCs) are in place for key financial reports, estimates, and footnote disclosures presented to investors.

Fraud Risk Management — Evaluate the company's fraud risk assessment, anti-fraud programs, and detective controls such as anomaly monitoring, audit logs, and exception reporting.

Documentation & Evidence Retention — Ensure that control owners maintain sufficient, timely evidence (screenshots, approvals, logs, sign-offs) to demonstrate that controls operated effectively during the audit period.

Management Review & CEO/CFO Certifications — Confirm that senior leadership has reviewed internal control assessments and is prepared to sign Section 302 and Section 906 certifications as required by SOX.

Remediation of Prior Deficiencies — Verify that any material weaknesses or significant deficiencies identified in prior audits have been formally remediated and re-tested.

Third-Party & Vendor Controls (SOC Reports) — Obtain and review SOC 1 Type II reports from key service providers whose systems impact financial reporting to assess outsourced control environments.

How to Perform SOX Compliance Audits

Here’s a comprehensive guide on how to conduct SOX compliance audits:

Phase 1: Planning and Walkthroughs

Update the risk and scoping assessment — review changes to the business, IT environment, and financial reporting since the prior year. Identify new entities, processes, systems, or significant transactions that may affect scope.

Refresh process documentation — update flowcharts, narratives, and risk and control matrices (RCMs) for all in-scope processes. Confirm with process owners that documentation reflects current operations.

Conduct walkthroughs — for each in-scope process, trace one transaction from initiation through recording in the general ledger. Walkthroughs confirm that documentation is accurate and support evaluation of control design.

Assess design effectiveness — determine whether each key control, if operating as designed, would prevent or detect a material misstatement. Document the rationale. Design deficiencies identified at this stage should be remediated before operating effectiveness testing begins.

Coordinate with external auditors — agree on the scope of internal audit testing that external auditors will rely upon, the level of direct assistance, and planned timing of deliverables.

Phase 2: Testing Operating Effectiveness

Operating effectiveness testing verifies that controls have functioned as designed throughout the audit period — not just at a point in time. Using audit management software can help teams centralize evidence, track sample populations, and maintain consistent testing documentation across all in-scope processes.

Testing strategies by control type:

Control Type | Typical Test Approach | Sample Size Guidance |

Manual preventive (e.g., approval of journal entries) | Inspect evidence of performance (signatures, system approvals) | 25–60 samples depending on frequency |

Automated control (e.g., system access restriction) | Test once + verify IT general controls support | 1 test + ITGC reliance |

Detective control (e.g., management review of variance analysis) | Inspect documented reviews and evidence of follow-up | 2–5 samples for quarterly; 1–3 for annual |

Entity-level control | Inquiry + observation + corroborating evidence | Judgmental |

Key testing considerations:

For controls operating daily or weekly, sample sizes are typically drawn from the full population for the period under audit — not just Q4.

Roll-forward procedures are required when interim testing is performed: controls must be tested from the interim date through year-end, or the auditor must gain comfort that the control continued to operate effectively.

Information Produced by the Entity (IPE) — any report or system-generated data used as evidence must be separately validated for completeness and accuracy. This includes confirming the report parameters, data source, and that the population is complete. IPE failures are a common source of PCAOB inspection findings.

Phase 3: Deficiency Evaluation and Remediation

Deficiencies identified during testing must be evaluated individually and in aggregate:

Control deficiency — the design or operation of a control does not allow management or employees to prevent or detect misstatements on a timely basis.

Significant deficiency — a deficiency, or combination of deficiencies, that is less severe than a material weakness but important enough to merit attention by those responsible for oversight.

Material weakness — a deficiency, or combination of deficiencies, such that there is a reasonable possibility that a material misstatement would not be prevented or detected on a timely basis. Material weaknesses must be disclosed in the annual report.

Remediation requirements: For each deficiency, document the root cause, the remediation action, the control owner, and the target remediation date. Retesting is required to confirm that the remediation is operating effectively before management can conclude that the deficiency is closed.

Phase 4: Management Assessment and Reporting

Management's assessment report — describes the ICFR framework used (COSO), the scope of the assessment, testing results, any identified material weaknesses, and management's conclusion on ICFR effectiveness. Filed as part of the annual 10-K.

CEO/CFO certifications (Section 302) — certify the accuracy of financial statements and the effectiveness of disclosure controls and procedures. Required for each annual and quarterly filing.

External auditor attestation (Section 404(b)) — required for accelerated filers. The external auditor independently tests and issues an integrated opinion on both the financial statements and ICFR under PCAOB AS 2201.